$5 minimum deposit online casino

$5 minimum deposit online casino

Do you know what market you are investing in? Is it the Tangible Primary? or the Intangible Secondary? The latter is a very bad choice.

NEW - Fraud on the court. How is an investment whole if parts of it are scattered among the years? Are you really getting your investment, or are you getting a box of bricks?

A

look inside your carrot? From a well known name in the latest credit

card scam. Credit card, electronic note, is there really a difference in

the scam?

A

look inside your carrot? From a well known name in the latest credit

card scam. Credit card, electronic note, is there really a difference in

the scam?

$5 minimum deposit online casino

This is a living website being updated when the Spirit moves upon the living waters, or if newsworthy articles are available to help you. However, there are plenty of articles and charts to help you, if you are not to lazy to find out.

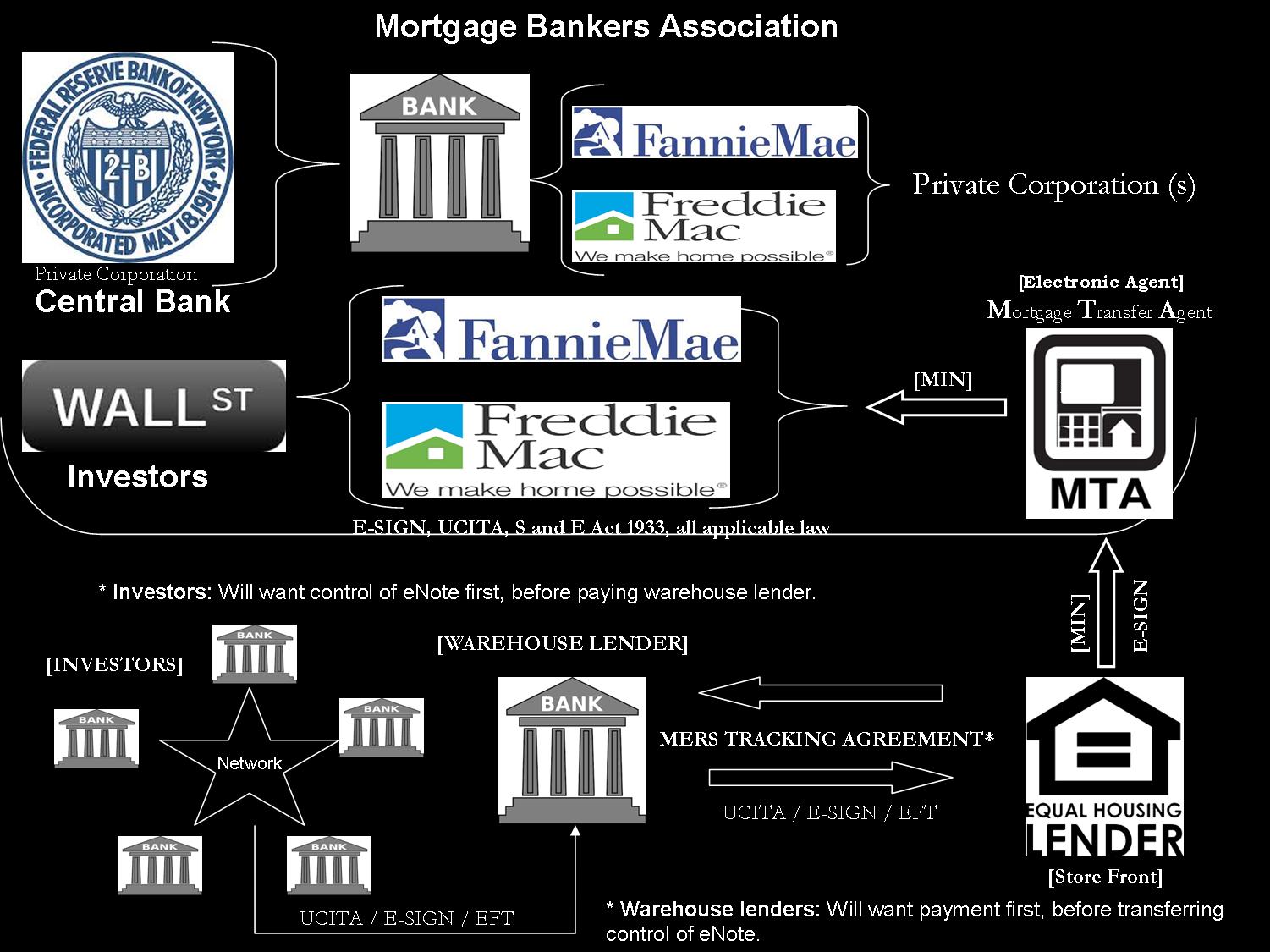

This was probably pitched to you at some point. Maybe not in the same way as the following excerpt out of the MERS foreclosure guide, but you were probably given the idea you possibly hold the homeowners note as your investment?

The agencies' policy is that the promissory note is endorsed in blank when the seller/servicer sells the loan to them. Therefore, the note should rem ain endorsed in blank when the foreclosure is commenced in the name of MERS. We have been advised that sometimes the Note is endorsed to the servicer prior to the foreclosure, but unless it is legally required, the Note should remain endorsed in blank. MERS stands in the same shoes as the servicer to the extent that it is not the beneficial owner of the promissory note. An investor, typically a secondary market investor, will still be the ultimate owner of the promissory note.

Yep, Mr. investor, they say you will be the "ultimate" owner of the promissory note. The note is a promise to pay, but since MERS has the deed of trust, they get the land. Comprende? You hold a piece of personal property, excluding the real property. That is the carrot for you. But, your servicer is out flipping the real property for a profit and provides you with what you deserve. You hold the note, the book entry sysstem holds the mortgage, so they say. Want to blame someone? Blame it on the lawmakers. They allowed MERS to use you as an "unknown" party to their crimes. Has tax evasion ever came to your mind? You may even want to scrutinize the note because of electronic laws. Once converted to paper, it is paper, not electronic. You can't rescan it. And another thing for you to think about? Can you support your argument of a converted electronic contract; and can that electronic contract meet the requirements of Article 3, negotiable instruments? According to what they say, don't you realize you own the note? So, where is the chain of the "unknowns" whom sold it to you? Securitization is a step process. Each step, laws were to control such actions in the step, including local law of jurisdiction. They missed many laws in the steps to get you your electronic note. But then again, who know whom the investor is? It is easy to make things up. Isn't that what the justice depaartment found out? Where are the investors? Imagine that, an imaginary stock market?

Have you ever read "Anatomy of an eNote"?

Do you realize that the "collateral" for your investment, lacks the value you believe it does? A lot of corners were cut to speed up the process of securitization of real estate mortgage loans. The "security" lost its value along the way. It's a long story, but practically every mortgage the agencies like VA, FHA, Ginnie Mae, required, and were required by Texas law to record its "interest" in deed of trust in public records where the real property is located. After that, Texas law also required every document affecting the deed of trust must be recorded thereafter. By failing to adhere to such laws, is it very possible these governmental agencies were defrauded, in one form or another? You may not be interested in researching it for yourself, that is your choice. After all, the stock market is a gamble? Just like electronics, here today, gone tomorrow?

Another problem exists with the conversion of the borrower's promissory Note, to what is said to be the electronic promissory note registered in the MERS system, the special purpose vehicle, for alleged real estate into the Secondary, intangible Market. If the individual how claims there is an original Note, you really should persuade them to prove it to you because you are investing in it right? And you would probably realize that you can't stick you nose into third party business, right? It was designed to be that way.

In other worlds, if the underlying security you are investing in for a "return" could not be proven by law that it was a "security", legal, under U.S. law, both state or federal, would that make you an accessory to a crime? Tax evasion, possibly?

You may come to find more than just "real estate" is involved in this eScam

There actually are a few movies out there that speak truth about this debacle. In essence, here is what happened to you the investor, wherever, whomever you are?

$5 minimum deposit online casino

The banks created empty trusts and then sold shares in those trusts to investors (i.e., pension funds).

This "information" about the 401k's, pension plans, etc., being used as "investors" can be found in an "agricultural" hearing a few years back. I don't suppose anyone saw that on CSPAN? You just need to look for it, and you will find it.

Instead of funding the trusts, the eSchemer's kept the money from the investors and made as few loans as possible to cover their tracks. And to make sure they would make even more money they made the worst possible loans that were certain to fail and thus gave themselves a sure thing on which to place multiple, layered bets. Some call it insurance. PIP profits, you might say.

In order to close the loop the eSchemer's needed as many loans as possible to be foreclosed, regardless of whether the property owners were current in their payments or not and in order to make that a very certain thing, they arranged it so that "servicers" with contracts with the empty trusts, stepped in and acted like servicers and are taking money that nobody owes them or the trust, because the trust never bought the loan because the trust was never funded.

This was where eSchemer's like Barrett Daffin Frappier Turner & Engel, and its associates across the country were able to help various "government" agencies misunderstand MERS, and to modify "property" codes across the country to allow the MERS systems to create and record fraudulent "assignments" as evidenced by those of Stephen C. Porter, Tommy Bastian, David Seybold, and the many others who filed such fraudulent recordings into public records in Texas for their monetary gain. To top it off, it was admitted in a Texas Supreme Court "task force meeting" that documents were made up to help the crime because the documents did not exist. Not only that, but lawyers like Mark D. Hopkins, Austin Texas, has added as much as 30 extra words to existing court opinions, to gain favor from the court, even though this was brought to the attention of the Texas Attorney General, and the dismal Texas court system of various men in robes who've ignored the fact. It is a matter raised and evidenced in Texas court records. Thus ill-faded men in robes committed crimes by association.

Next, modifications were utilized to lure the unsuspecting homeowners deeper and deeper into the illusion of a default. The default never existed because like in any Ponzi scheme the real owners of the debt (the investors) in this eScheme were always getting paid regardless of whether the "borrowers" ever made a payment. It is said, "If you tell a lie long enough, you will convince them, and they will believe it to be true".

$5 minimum deposit online casino

Investors were getting paid from a slush fund. Each payment was labeled a servicer advance, when the servicer was not authorized as a servicer, which didn't make the payment, and didn't even cause the payment to be made because that was the task for the hidden "Master Servicer", the bank that created the fake trusts and conducted fake sales of shares in the fake trusts.

Nevertheless, that didn't stop the banking "actors" from foreclosing in record numbers, inherently inundating public records with trustee sale recordation's, thus confusing the borrowers; and influencing the courts enough with lies that everyone thought it must be true that the "banks" were the lenders . That is, until everyone finds out these criminals were not lenders. They were brokers at best and thieves at worst.

Have you ever heard the phrase "Useless as tits on a boar hog", or "Useless as tits on a Bull"? think about those phrases until I get back? Need any wooden nickels?

Maybe this is why public banking is far better than national banking?

Pay attention to this video, you may learn something about your investment.

Other videos, or links, are on the videos page.Quando você entra na arena ou –$5 minimum deposit online casinoqualquer coisa que você se destaca – você está lá para fazer o trabalho que deve ser feito. Não importa o quão longe você está de mim.

For your Remic understanding

When will you, the investor understand? Are you blinded because "funds" keep coming to you from you RMBS investment? Do you realize you are a part of the criminal activity? You should look closer into your "investment".

This link will probably change so, be prepared to look for it yourself. The title of the article is "Ocwen Closes Servicing Advance Securitization Worth $600 Million".

In the article it states

"The notes are used to finance the servicing advances that are used to fund RMBS investors, according to an Ocwen spokesman, who also noted that the company believes the securitization of the advances is the most efficient and lowest cost form of borrowing available to mortgage servicers."

In essence, the entities like Ocwen, though there are many others, are selling, and reselling "promises to pay", from electronic images to make you believe there is actually money coming to you from a Residential Mortgage Backed Security", when the truth of it all is the RMBS is a Registered Mortgage Backed Security. Those monies come from victims of the scam. A whirlwind of intangibles payment streams from fictitious real property mortgage loans which are bifurcated, thus stripped of its "Securities", both the value of the Note, [§3.302(d)] and the "deed of trust", a lien governed by certain laws. Though your "intangible" is considered legal, it is unsustainable. Are you prepared to be last?

This criminal scheme is designed to keep the investor, homeowner, public records, courts, people, media, the world, divided for the scheme to go unnoticed. Have you ever looked at the definition of "greed"?

There are enemies within....

Look at it this way, a person who is a carpenter, works with fine wood. He goes through all the pangs of detail for his fine craftsmanship. A person whom claims to be a carpenter, only knows how to cover up his shoddy woodwork so there is only an appearance of fine wood, because he never paid attention to the fine details it takes to make a fine piece of woodwork worth its weight in value, even though he claims to be a carpenter.

The world is running around its fist to get to its thumb.

Take this into consideration for your "valued" investment. 15 USC 77nnn?

It is being revealed to the world that the members of a certain "mortgage" registration system, caused many laws to be bypassed in order to stuff the secondary intangible market via the electronic highway.

If the "securities" were not true securities; how would a "Trustee of a a certain Trust" lawfully hold a capacity, or have standing in a court of law? It is all about abiding by the law, correct?

In God We Trust

May this will help you get it?