MERS, Members, E-SIGN, UCC and the one-sided affair

NOTE; DEED OF TRUST = Aka "Secured debt"

I'm not going in to detail about this portion simply because it is already written in many other articles. What I will do is explain with a few laws to better understand what MERS members didn't do, and how they really can't do what they continue to do. I will be primarily be using Texas law, but the UCC can be found in most states statutes. So can E-SIGN, or UETA.

The U.C.C. excludes liens, such as a deed of trust. You can find that in §9.109

The deed of trust may be recorded in public records. You can find that in Chapter 11, Texas Property Code

For purposes of "entitlement", the deed of trust is recorded, even though it is not required. Once the deed of trust is filed, recorded into public records of a county, local law of jurisdiction become effective. You can find that in Chapter 192, Texas Local Government Code.

THE TRAP

Homeowners are in a realm of purchasing a home for their future. MERS is not something they are aware of. They only know they have a lot of paperwork to sign at closing for their "dream home". Once completed, the future homeowner only need to make his/her payments monthly and in years to come, when paid in full, the home becomes theirs without debt of the mortgage payments. That is the "dream". Did the homeowner know the contracts they were to sign were contracts of adhesion? If they had an attorney review the contracts, did the attorney know these were contracts of adhesion? I believe the attorney no more realized the contracts were unconscionable than the people presenting them for the closing of the real estate mortgage loan. Think about it, how can you keep a secret if everyone knows?

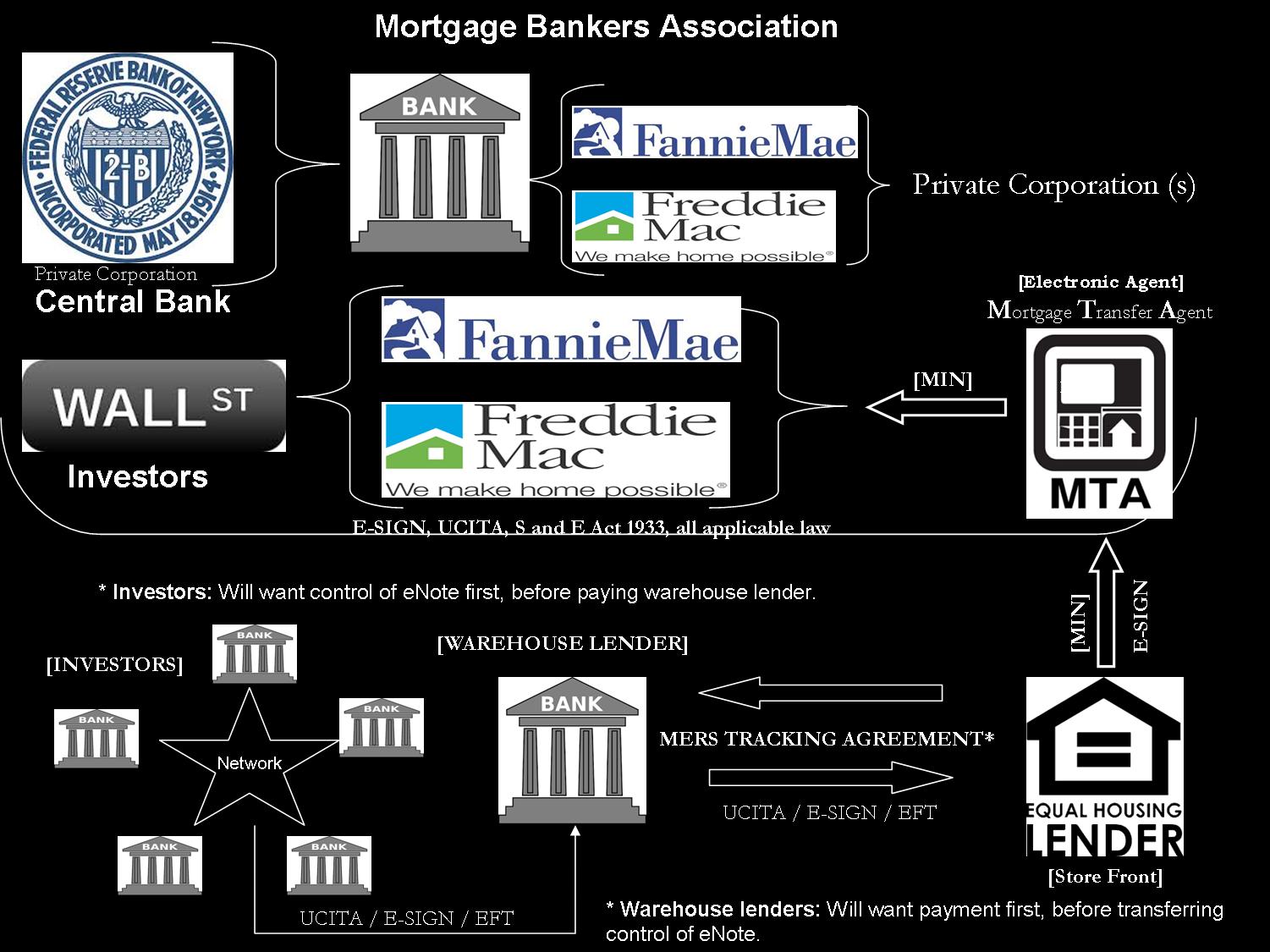

I've used this illustration on another page but review it for a moment;

Do you see any association? What "deed of trust" is used? Is it a GSE "deed of trust"? Is it a government entity "deed of trust"?

Whomever it was that constructed the crafting of words within the GSE's "deed of trust", was associated with the "Association". And how was the government talked into placing the "MERS" wording in its deed of trust? Contracts seem to have a history of be "one-sided" for the party constructing the contract, but this "word crafting" has taken a new height to the meaning of "one-sided". So much, not even the courts, nor the government seem to catch this scam? Or they are turning a blind eye? I am not the judge. That is their cause.

MERS- Mortgage Electronic registration Systems, Inc.

Tell me what MERs is? Is it a "beneficiary" Is it a "nominee"? It is for MERS members. Take a look at a MERS electronic tracking agreement. When you do look at the multiple eAgreements take notice to the parties. In two of the agreements, "Whole loan", and "Gestation" the parties are seller and purchaser; and in the "Wholesale Lender" the parties are "Lender" and "Borrower". So when the MERS members claim the borrower agreed, they are actually telling the truth. Only the need for clarification is required as to "what lender", and "what borrower" are the MERS members referring to? These "members" know you are too ignorant to see what they are doing. Once you realize you are looking at a Stereogram, you will notice the elephant in the room. You do know what a stereogram is, right?

Why is MERS a beneficiary, or nominee? Let's look at some definitions to help;

Beneficiary - a person who derives advantage from something, especially a trust, will, or life insurance policy.

Nominee - a person or company whose name is given as having title to a stock, real estate, etc., but who is not the actual owner.

Since corporations are allegedly considered "persons", MERS can easily fit either definition. But MERS is a different kind of person. MERS has no personality, only bits & bytes. Yes MERS is a corporation. Many "securitization" vehicles are created as corporations under the laws of Delaware. How many court cases come forth using some "Trust" in which MERS was involved? I suppose this could be part of the confusion?

One other thing to mention about the electronic tracking agreements, who is the "electronic agent"? The Association seems to have left an opening in their representation of MERSCORP Holdings, Inc. Can it be explained how Primary corporation is an electronic agent, and the other corporations are subsidiaries? As presented, MERSCORP Holdings, Inc. is the parent company of Mortgage Electronic Registration Systems, Inc. Logically thinking, what would Mortgage Electronic Registration Systems, Inc. be in relationship to MERSCORP Holdings, Inc. if MERSCORP Holdings, Inc. is an electronic agent as defined in 15 USC 7006;

(3) Electronic agent The term “electronic agent” means a computer program or an electronic or other automated means used independently to initiate an action or respond to electronic records or performances in whole or in part without review or action by an individual at the time of the action or response.

The whole MERS debacle is based upon misleading, and misguided information. In other words, false information. False claims of what the MERS system actually is and what it can do.

Look at the massive amounts of void judgments or opinions issued by ignorance of the courts, you'll find in each one MERS is described as a system which tracks beneficial interests and servicing rights of eNotes registered by its members. Have the courts ever mentioned that MERS does not track beneficial interests in the homeowner's paper promissory note, when MERS clearly states the registration system does not track paper notes, only eNotes. you can find that in "National eNote Registry, Requirements Document, Version 1.0, Mar 7, 2003"

e. The National Registry functionality is limited to electronic notes, and not paper notes. [Section 5; Key Assumptions]

If the MERS system does not track the paper note, why do the courts continue to allege MERS does?

The MERS system is "an electronic mortgage registration system and clearinghouse that tracks beneficial ownerships in, and servicing rights to, mortgage loans." In re Mortg. Elec. Registration Sys. (MERS) Litig., 659 F. Supp. 2d 1368, 1370 (J.P.M.L. 2009).

That is all the MERS system does. So, if it is only a system for "registration, and tracking", what is being tracked? Answer; Personal property mortgage loans registered by MERS members. These personal property mortgage loans contain images of homeowner mortgage loans, not actual paperwork from the real estate mortgage loans. How can you convert paper to electronic? Scanner? But with Article 3 Notes, scanning does not work to meet the requirements, other than counterfeiting.

How about this statement;

The MERS® System is not a legal system of record, nor a replacement for the public land records. No interests are transferred on the system; they are only tracked.

Is that claim a bit oxymoron? No interests are transferred on the system? When servicing rights, or beneficial rights are sold, purchased, transferred, or assigned, there is no interest transferred? What is the purpose of the MERS Milestone report then? However, if you recognize this statement, MERS is admitting that no matter how many ineligible assignments are recorded into public records, "No interests were transferred" in the paper promissory note. Only interests in the eNote.

Honestly, I am a bit tired of the courts using the void opinion from my litigation, to defeat other homeowners. These men in robes should be ashamed of themselves for being so ignorant. I do forgive them, but their ignorance is evident. And I will state that High Court in Tennessee seems to be the closest in understanding MERS. But if the court had really understood the MERS system, I believe its opinion would have been way different and more devastating to the MERS members than what is was. Then you have MERS attempting to make a big deal out of a Texas district court opinion that MERS has rights to notice of lawsuit. Geez. Most should realize the district court opinion does not carry much weight. And again, ignorance is no excuse for the court.

So, if MERS members were to conduct business electronically in the MERS system, these electronic transactions are governed by E-SIGN, solely. No UCC, except for Article 2, Sales, nor anything else excluded by E-SIGN as noted in 15 USC 7003.

Here is an exhibit posted on stopforeclosurefraud.com to help with my explain. Why? Because the courts state that MERS only tracks "rights". But, according to MERS corporate resolution, MERS corporate officers can accomplish the following;

Execute any and all documents necessary to foreclose upon the property securing any mortgage loan registered on the MERS System that is shown to be registered to the Member, including but not limited to (a) substitution of trustee on Deeds of Trust, (b) Trustee's Deeds upon sale on behalf of MERS, (c) Affidavits of Non-military Status, (d) Affidavits of Judgment, (e) Affidavits of Debt, (1) quitclaim deeds, (g) Affidavits regarding lost promissory notes, and (h) endorsements of promissory notes to VA or HUD on behalf of MERS as a required part of the claims process;

Question? If only "beneficial interests" and "servicing" rights are tracked on the MERS system, and the paper promissory note is not tracked, why does a MERS corporate officer have power to do the following? Was the note endorsed to MERS? How would MERS endorse a note? Would that not be up to the note owner's agent?

(g) Affidavits regarding lost promissory notes, and (h) endorsements of promissory notes to VA or HUD on behalf of MERS as a required part of the claims process;

WHOM SCREWED WHOM?

MERS Loan scam

MERS Loan means a loan for which MERS is the mortgagee , beneficiary, grantee , nominee of the lender , or other secured party .

Why is it so important for this bankruptcy remote to be the mortgagee of record? Is it easier to separate the deed of trust away from the paper promissory note using the MERS slice and dice? I still cannot comprehend how this has not been recognized by the various court by now. Was law completely thrown out the window? MERS has no functionality whatsoever to track a paper promissory note, but it has the functionality to track the deed of trust. So, in essence by MERS own statements, claims, instructions, admissions, the deed of trust is separated from the paper promissory note because MERS does not have the functionality to track the paper promissory note, only the deed of trust. And the sad thing about it is nobody is paying attention to that certain wording within the four corners of the deed of trust which makes it so one-sided.

If MERS members wanted to sell bits and pieces of its interest in, the MERS member did not need MERS to accomplish that.

Back to business

So, what you may come to see is; GSE, or government entity "deed of trust" are utilized for real estate mortgage loans. These entity deed of trust require MERS to be named within the deed of trust, MERS requires MERS to be named within a deed of trust according to its membership, rules, procedures, and electronic tracking agreements. without the use of MERS, you will not obtain a GSE type loan. One-sided, and unconscionable contracts cannot be upheld according to the various courts. Contracting to commit a crime is against the law too.

So, just exactly how did the potential homeowner agree to using MERS in a deed of trust? Assent by silence? Silence by Estoppel? Ignorance? Misrepresentation? Fraud? Inducement to unknowingly commit a crime?

So, when it is understood about MERS, many questions will come to mind. Like the corporate resolutions used by alleged foreclosure mills across the state, and country. How does the foreclosure mill contract with an "electronic agent", a shell corporation, a bankruptcy remote, a securitization vehicle, created under the laws of Delaware? Better yet, how did the "electronic agent" know to contract with the foreclosure mill? MERSCORP Holdings, Inc. is the primary electronic agent. According to MERS website, MERSCORP Holdings, Inc. the "electronic agent", is the parent company to the "software" Mortgage Electronic Registration Systems, Inc., with MERS identified as a variable. All called "MERS Entity" according to MERS rules of membership.

For grins and giggles, maybe you should review the MERS system rules of membership? Maybe pay attention to the "MERS as Mortgagee of Record" part. The note being mentioned is the eNote, not the paper note because MERS does not track paper notes. You do know there is no U.S. law to support the electronic promissory note, other than E-SIGN. Article 3 is excluded from E-SIGN, see 15 USC 7003. Which means that even if the electronic promissory note were converted into paper, it would not meet the requirements of negotiability in Article 3. And if you were paying attention to my scenario about the "trusted source", you would realize that according to Article 3, in particular, §3.203(d), you would find that I could not transfer part of the note, much less part of the deed of trust.

How about the MERS Procedures manual? Page 85 begins with how a MERS members transfers interests in rights, which MERS claims it does not do. Put it this way, if the investor is the holder of the note with a beneficial interest, and beneficial rights are transferred to another investor, that is transferring an interest in rights. Or it could be just like the example I provided about "partial interest"?

You'll pick up on this eScam soon?

Have you ever read ""Seek But You May Not Find": Non-UCC Recorded, Unrecorded and Hidden Security Interests Under Article 9 of the Uniform Commercial Code" - Gerald T. McLaughlin

This is a living page, as the Spirit moves upon the living waters, so shall the fingers move upon the keyboard to update this site.

Let the world rejoice in your name, Lord Jehovah!

Namaste,